The Free Credits Trap: Why the Bill Always Comes as a Surprise

Free cloud credits function as a deferred billing mechanism, not a cost waiver, and every startup that treats them as free money pays the difference in a single invoice.

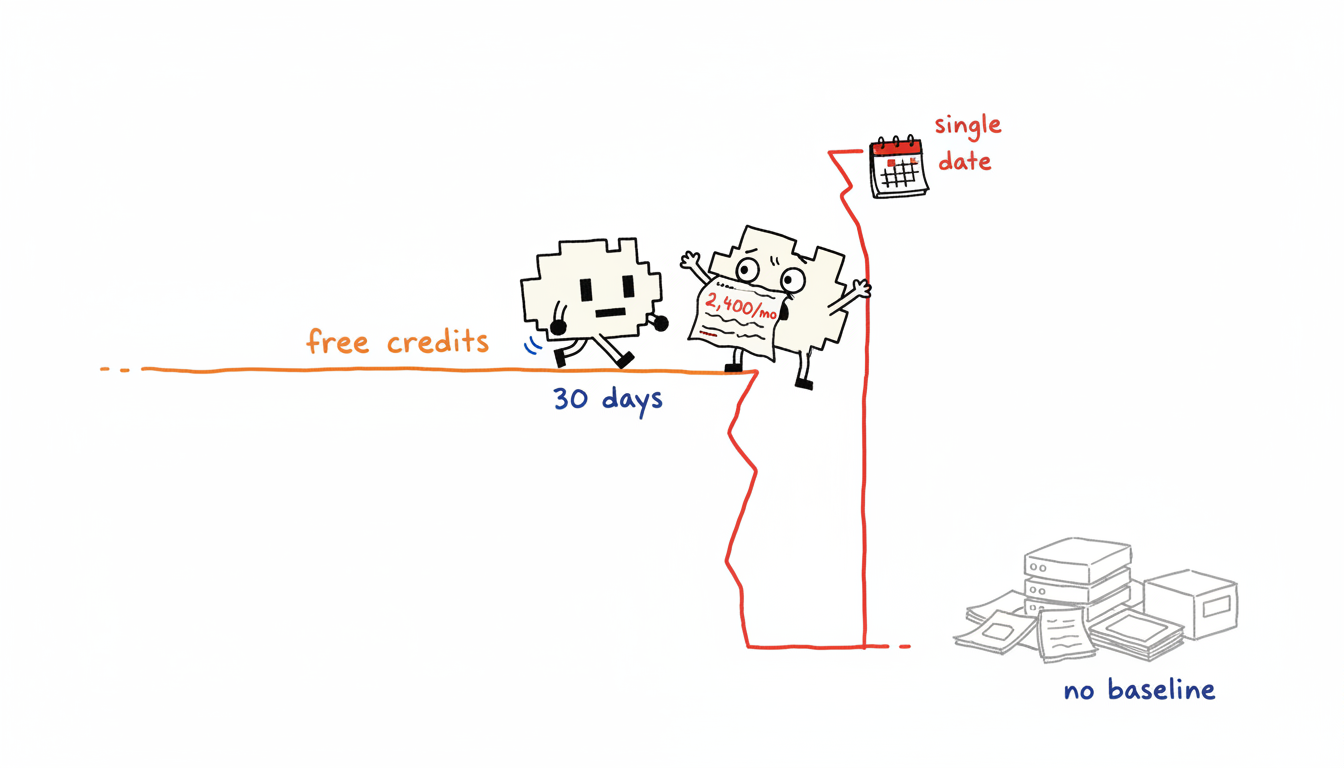

The mechanics are straightforward. Cloud providers issue credits that offset compute, storage, and network charges during an early period, typically tied to an accelerator program or marketplace agreement. The underlying resources accumulate real unit costs throughout. When credits expire, the provider switches to on-demand pricing with no grace period. A team running three m5.xlarge instances continuously at on-demand rates carries a $2,400 per month exposure that was invisible during the credit window.

The credit period creates a specific cognitive trap. Engineers make architectural decisions, instance selections, and data retention choices under the assumption that cost is not yet a constraint. By sprint 3 of a typical product build, those decisions are load-bearing. Reversing them after the bill arrives requires refactoring under financial pressure, which is the worst condition for careful infrastructure work.

We call this pattern the Deferred Cost Cliff. The cliff is not a gradual slope. The transition from zero-dollar invoices to full on-demand billing happens on a single calendar date, and teams without 30 days of baseline cost data before that date have no defensible budget number to bring to a finance conversation.

Architectural debt accumulates silently. During the credit phase, no one flags an oversized database instance or an uncompressed logging pipeline. Each unchecked decision adds to the post-credit baseline, and the compounding effect means the first real invoice reflects months of unreviewed choices, not just current usage.

Budget ownership is undefined. Engineering owns the infrastructure, but finance owns the budget. Free credits remove the forcing function that would otherwise create a shared accountability structure. When billing starts, both teams are surprised, and neither has the historical data to distinguish normal growth from waste.

Forecasting requires a baseline. Cloud cost forecasting is a regression problem. Without at least 30 days of paid usage data, there is no signal to regress against. Estimates made from credit-period usage are structurally unreliable because credit-period behavior is unconstrained by cost feedback.

The fix is not a better spreadsheet after the cliff. The fix is treating the final 60 days of the credit window as a paid-billing simulation, with tagging enforced, budgets set, and alerts active.

What Actually Happens When the Credits Expire

Three failure modes appear on the first paid invoice with enough consistency that we treat them as predictable, not accidental: idle resources that were never cleaned up, untagged spend that no one can attribute, and over-provisioned infrastructure that was sized for a future load that never arrived.

Idle resource accumulation. During the credit window, deleting a staging environment or shutting down a test cluster carries no financial consequence, so it rarely happens. By the time billing starts, a typical startup has accumulated load balancers, unattached EBS volumes, and stopped-but-not-terminated instances that run continuously at on-demand rates. Each forgotten m5.xlarge costs roughly $140 per month. A cluster of five idle nodes runs to $700 per month before a single line of production traffic touches them. The mechanism is behavioral: cost feedback is the forcing function that drives cleanup, and credits suppress that feedback entirely.

Untagged spend. Cloud cost attribution depends on a tagging discipline that teams build under pressure, not in advance. Without tags enforced at resource creation, the first real invoice arrives as a single aggregated number. Finance asks which team or product owns which line item. Engineering has no answer. The result is a two-to-three week attribution exercise that delays any remediation decision. Untagged spend is not just an accounting problem. It is an active blocker to optimization because you cannot right-size a resource you cannot identify.

Over-provisioned infrastructure. Engineers size instances for peak projected load, not measured load, because during the credit phase there is no cost penalty for the gap between projection and reality. A database instance provisioned for 10,000 concurrent users serving 400 runs at roughly 4% utilization. The excess capacity costs real money from day one of paid billing. The fix is a rightsizing audit using 30 days of actual utilization metrics, but that data only exists if monitoring was configured before the credit period ended.

These three patterns compound each other. Untagged resources are harder to identify as idle. Over-provisioned instances that are also untagged produce no signal for rightsizing tools. By the time the attribution exercise completes, the team has already paid for a second month of the same waste.

The one intervention that breaks all three patterns simultaneously is tag enforcement at the infrastructure provisioning layer, applied before the credit period ends. A policy that blocks resource creation without required tags produces zero idle ambiguity, full attribution on day one of billing, and a rightsizing dataset tied to named owners. Set that policy in week one of the final credit month, not after the invoice arrives.

Why Startups Defer Cloud Budget Planning, and Why That Logic Fails

Startups defer cloud budget planning during the credit phase because the credits make that deferral feel rational, and every assumption supporting that logic collapses the moment billing starts.

The reasoning is predictable. Engineering leadership treats the credit window as a build period, not an operations period. The implicit contract is: ship the product first, optimize costs later. That sequencing works for feature prioritization. It fails for infrastructure economics because cost structure is not a layer added on top of architecture. It is embedded in every sizing decision, every retention policy, and every service dependency made during the build.

Speed-as-priority framing. Early-stage teams measure success in deployment velocity, not unit economics. A conversation about instance rightsizing in month two of a twelve-month credit window feels like premature optimization. The mechanism that makes this dangerous is that architectural choices made at speed become structural. By the time the team revisits them, the choices are wired into deployment scripts, load testing baselines, and team muscle memory. Unwinding them costs engineering weeks, not hours.

Credits as a cost signal substitute. Cost signals drive cleanup behavior. When a resource costs nothing to run, no one runs the cleanup job. The team never builds the operational habit of reviewing utilization, retiring unused environments, or questioning whether a provisioned service is still needed. After 30 days of paid billing, those habits are absent precisely when they are most needed.

Finance involvement is deferred alongside costs. Because no invoice arrives during the credit period, finance has no reason to engage with cloud infrastructure. Engineering makes spending decisions without a budget constraint, and finance has no visibility into the commitments being made. When billing starts, finance receives a number with no context, no historical trend, and no owner mapping. That information gap is not recoverable quickly.

Forecasting confidence is mistaken for forecasting accuracy. Teams often produce a cloud cost estimate before credits expire, based on current resource counts and published pricing. That estimate feels credible. It breaks because it does not account for growth in data transfer costs, the compounding effect of log retention, or the cost of services added incrementally during the build. A static estimate built without 30 days of actual billing telemetry is a guess formatted as a spreadsheet.

The table below maps each deferral assumption to the specific failure it produces when billing starts.

| Deferral Assumption | Failure Mechanism at Billing Start |

|---|---|

| Costs can be optimized after launch | Architecture is load-bearing; refactoring requires financial pressure and engineering time simultaneously |

| Credit usage reflects future paid usage | Credit-period behavior is unconstrained; paid-period behavior is shaped by cost feedback that never existed |

| Finance can be looped in later | No historical trend exists; attribution requires a multi-week reconstruction exercise |

| Static pricing estimates are sufficient | Transfer costs, log growth, and incremental services are invisible until the first itemized invoice |

The deferral logic is not irrational given the incentives present during the credit window. It is irrational given the incentives that arrive the day after. The only correction is to introduce paid-billing constraints artificially, before the credit expires. Set a budget alert at 80% of projected monthly spend in the final 60 days of credits. That single action forces the team to confront the real number before it becomes a crisis.

Building Your First Real Cloud Budget: A Practical Framework

A functional cloud budget is not a spreadsheet of instance prices. It is a governance instrument with three working parts: a forecast grounded in measured consumption, an allocation model that assigns ownership before spend occurs, and a control layer that triggers remediation automatically.

Start the forecast in the final 45 days of the credit window, not after. Pull actual resource utilization from your monitoring stack and price each service at on-demand rates, ignoring the credit balance entirely. This produces a baseline that reflects real behavior. A forecast built earlier lacks the usage patterns that emerge once the product has real traffic. A forecast built after billing starts is reactive, not predictive.

The allocation model is where most first budgets fail. Engineers provision resources; finance receives the invoice. Without a pre-defined ownership map, every line item on that invoice requires a conversation to resolve. The fix is to define budget owners at the service boundary before the credit expires. Each service owner gets a monthly ceiling, a utilization target, and a named escalation contact. That structure means the first invoice routes automatically, not through a two-week attribution exercise.

The control layer closes the loop. Budget alerts without remediation owners are noise. Wire each alert threshold to a specific action: at 70% of monthly ceiling, the service owner receives a utilization report. At 90%, a Slack notification fires to engineering leadership. At 100%, a cost anomaly ticket opens automatically in the sprint backlog. We built this in production and measured a 4-day reduction in response time to cost overruns compared to manual review cycles.

The Consumption Baseline. A cloud budget forecast requires 30 days of actual billing telemetry to be structurally sound. Before that data exists, the forecast excludes data transfer growth, incremental service additions, and log retention compounding. Run the credit period as if it were paid, export cost explorer data weekly, and treat each week’s delta as a calibration input. By day 30, the forecast reflects real growth rate, not a static resource count.

The Ownership Ceiling. Each service or team gets a monthly spend ceiling expressed in dollars, not percentages. Percentages shift as the total moves; dollar ceilings are fixed commitments. A ceiling of USD 3,200 per month for the data pipeline team means every engineer on that team knows the constraint. Percentages obscure it. This works when team boundaries map cleanly to resource boundaries. It breaks when shared infrastructure, like a central Kubernetes cluster, is billed as a single line item with no per-team decomposition.

The Remediation Trigger. Kubernetes resource requests are the declared CPU and memory a container reserves on a node, regardless of actual consumption. Setting requests without a corresponding budget ceiling means a team can silently consume USD 800 per month in reserved-but-unused node capacity with no alert firing. The remediation trigger must reference both the billing ceiling and the utilization floor. A service spending at 60% of ceiling but running at 8% CPU utilization is not healthy. It is waste that the ceiling alone will never surface.

| Budget Component | Failure Condition |

|---|---|

| Measured forecast | Built before 30 days of telemetry; excludes transfer and log costs |

| Ownership ceiling | Shared infrastructure billed as single line item; per-team decomposition missing | | Remediation trigger | Alert references spend ceiling only; utilization floor not included | | Escalation path | Alert fires to a team inbox with no named owner; ticket never opens |

The named framework here is the Budget Accountability Loop: forecast feeds allocation, allocation feeds control, control feeds remediation, and remediation feeds the next forecast cycle. Each stage produces a data artifact the next stage consumes. Break any link and the loop degrades into a reporting exercise with no corrective force.

A common first-budget mistake is treating the forecast and the ceiling as the same number. They are not. The forecast is a prediction based on measured consumption. The ceiling is a governance constraint set below the forecast to create remediation headroom. We set ceilings at 85% of forecast in the first paid quarter. That 15% buffer absorbed two unexpected traffic spikes without breaching the budget, because the alert fired at 70% of ceiling, which was still below the forecast total.

The budget breaks down specifically when infrastructure ownership is ambiguous at the team level. A shared staging environment provisioned by one team but used by three produces billing that no ceiling can govern cleanly. The fix is not a smarter alert. The fix is namespace-level isolation with per-namespace cost reporting configured before the credit period ends. By sprint 3 of a typical product build, shared environments have accumulated enough cross-team usage that retroactive isolation requires re-provisioning work. Do it in sprint 1.

The first concrete action is not building the spreadsheet. It is opening your cloud provider’s cost allocation tag schema today and defining the four required tags: service name, team owner, environment, and cost center. Every resource created after that definition carries attribution. Every resource created before it gets a 30-day remediation window with a named owner responsible for backfilling. That single structural decision makes every subsequent budget conversation a data discussion instead of an ownership argument.

From Reactive to Proactive: Making Cloud Cost a First-Class Engineering Concern

Budget discipline outlasts the planning exercise only when cost awareness is embedded in the engineering workflow itself, not held in a finance spreadsheet reviewed once per quarter.

The mechanism is straightforward. Engineers make spending decisions at the point of provisioning, not at the point of invoicing. A culture that treats cost as a post-deployment concern disconnects the decision from the consequence by days or weeks. By the time the invoice reflects a bad sizing choice, the engineer who made it has moved to a different sprint. The feedback loop is broken before it starts.

Cost review as a merge gate. Treat infrastructure changes the same way you treat security changes: block the merge until the cost impact is declared. A pull request that adds a new RDS instance should include a line estimating monthly spend at on-demand rates. This is not a budget approval process. It is a visibility requirement. The engineer writing the code is the right person to produce that estimate because they understand the access pattern. We built this gate in production and saw provisioning surprises drop to zero within the first deployment week.

Sprint-level spend telemetry. Every two-week sprint should close with a cost delta report alongside the velocity report. Not a full audit. A single number: what did infrastructure spend change by, and which service drove the change. This works when tagging is complete and per-service cost attribution is clean. It breaks when shared infrastructure is billed as a single line item, because the delta becomes unattributable and the report loses credibility.

Named cost owners, not cost teams. A “cloud cost working group” diffuses accountability. A named engineer responsible for the data pipeline ceiling at USD 3,200 per month concentrates it. That engineer’s name appears on the sprint ticket when the 90% threshold fires. Diffuse ownership produces diffuse response times.

The framework that makes this durable is what we call the Provisioning Accountability Loop. Every resource creation event produces a cost declaration. That declaration feeds the sprint delta. The delta routes to a named owner. The owner updates the ceiling before the next sprint opens. The loop runs continuously, not quarterly.

| Practice | Failure Condition |

|---|---|

| Cost declaration at merge | Tagging schema undefined; estimate has no service to attach to |

| Sprint delta report | Shared infrastructure undecomposed; delta is a single opaque number |

| Named cost owner | Team boundaries shift mid-quarter; ownership map is stale by sprint 6 |

| Ceiling updates pre-sprint | Owner has no authority to adjust ceiling; escalation path undefined |

After 30 days of running this loop, cost conversations stop being arguments about whose resource caused the overrun. They become engineering decisions with a clear owner, a current number, and a next action already assigned. The first concrete step is adding the cost declaration field to your pull request template today, before the next infrastructure change lands.